WASHINGTON — National Taxpayer Advocate Erin M. Collins today released her statutorily mandated mid-year report to Congress. The report expresses concern about continuing delays in the processing of paper-filed tax returns and the consequent impact on taxpayer refunds. At the end of May, the agency had a backlog of 21.3 million unprocessed paper tax returns, an increase of 1.3 million over the same time last year.

“The IRS has said it is aiming to crush the backlogged inventory this year, and I hope it succeeds,” Collins wrote. “Unfortunately, at this point the backlog is still crushing the IRS, its employees, and most importantly, taxpayers. As such, the agency is continuing to explore additional processing strategies.”

The report points out that the significant majority of individual taxpayers receive refunds. “At the end of the day, a typical taxpayer cares most about receiving his or her refund timely,” Collins wrote. “Particularly for lower income taxpayers who receive Earned Income Tax Credit benefits, tax refunds may constitute a significant percentage of their household income for the year. Thus, these processing delays are creating unprecedented financial difficulties for millions of taxpayers and outright hardships for many.”

Among business taxpayers, many have been waiting extended periods to receive Employee Tax Retention Credits for which they are eligible, in addition to their regular refunds.

Key taxpayer challenges this year have included return processing delays, correspondence processing delays, and difficulty reaching the IRS by phone.

Backlog of Unprocessed Paper Tax Returns

More than 90% of individual income taxpayers e-file their returns, yet last year, about 17 million taxpayers filed their returns on paper. Some choose to file on paper. Some have no choice because they encounter e-filing barriers, such as when they are required to file a tax form or schedule the IRS cannot accept electronically. Before the pandemic, the IRS typically delivered refunds to paper-filers within four to six weeks. Over the past year, refund delays on paper-filed returns have generally exceeded six months, with delays of 10 months or more common for many taxpayers.

The report says the IRS has failed to make progress in eliminating its paper backlog because “its pace of processing paper tax returns has not kept up with new receipts.” During the month of May, the IRS processed an average of about 205,000 individual income tax returns (Forms 1040) per week. Its Form 1040 backlog at the end of May stood at 8.2 million, with millions more paper tax returns not yet classified or expected to arrive before the extended filing deadline of October 15. The report says the IRS would have to process well over 500,000 Forms 1040 per week – more than double its current pace – to eliminate the backlog this year. “The math is daunting,” the report says.

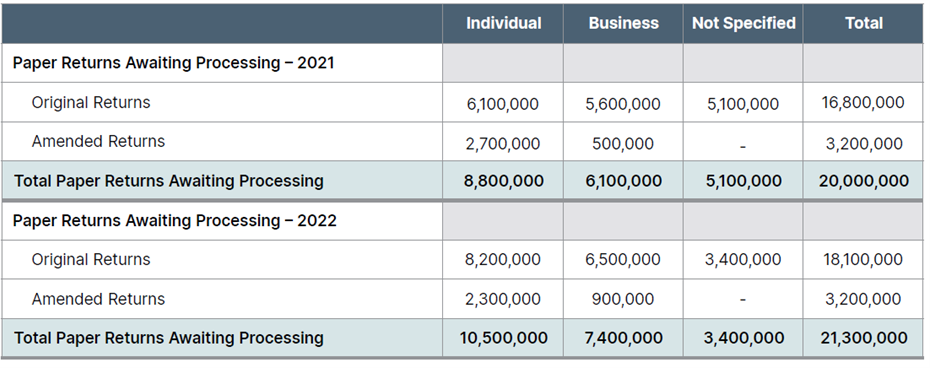

Forms 1040 are just one component of the paper tax returns processing backlog. Millions of business tax returns and amended tax returns (both individual and business) are also filed on paper. The overall backlog has increased by 7% over the past year as shown in the Figure 1.

Figure 1: Status of Unprocessed Paper Tax Returns Comparing Weeks Ending May 22, 2021, and May 27, 2022

The IRS has publicly committed to reducing its paper tax return backlog to a “healthy” level by the end of the year, but it has not provided a definition of “healthy.” “Historically, the IRS has paid refunds resulting from paper-filed returns within four to six weeks,” Collins wrote. “From a taxpayer perspective, returning to a four-to-six-week refund delivery period is a reasonable definition of ‘healthy.’”

Largely because of the likelihood that the IRS will carry a large inventory of unprocessed paper tax returns into the 2023 filing season, Collins issued a Taxpayer Advocate Directive (TAD) in March directing the IRS to implement 2-D barcoding or other scanning technology to automate the transcription of paper tax returns. “Today, the digits on every paper return must be manually keystroked into IRS systems by an employee,” Collins wrote. “In the year 2022, that doesn’t just seem crazy. It is crazy.” The IRS’s response to the TAD is due on June 27, 2022.

The report credits the IRS with taking recent steps to address the backlog but notes “missed opportunities” to have acted earlier. “The IRS’s paper processing delays were evident more than a year ago, and the IRS could have addressed them more aggressively at that time,” Collins wrote. “Had the IRS taken steps a year ago to reassign current employees to processing functions, it could have reduced the inventory backlog carried into this filing season and accelerated the payment of refunds to millions of taxpayers. Had the IRS implemented 2-D barcoding, optical character recognition or similar technology in time for the 2022 filing season, it could have reduced the need for employees to engage in the highly manual task of transcribing paper tax returns. Had the IRS quickly used some of the $1.5 billion of additional funds provided by the American Rescue Plan Act of 2021 (ARPA), which was enacted 15 months ago, to hire and train additional employees, it could have worked through the backlog, answered more taxpayer telephone calls and otherwise improved taxpayer service.”

At the end of May 2021, the IRS had an additional 15.8 million returns that had been suspended during processing and required manual review by IRS employees. The suspended returns consisted largely of

e-filed returns on which taxpayers claimed Recovery Rebate Credit amounts that differed from the allowable amounts shown on IRS records. As of May 2022, the IRS had reduced the number of suspended returns to 5.4 million. The report credits the IRS with developing procedures to reduce delays among suspended returns, in part by automating the review process. However, e-filed returns suspended during processing did not generally result in extended refund delays. By contrast, unprocessed paper-filed tax returns have resulted in refund delays of six to 10 months or longer.

Correspondence Processing Delays

When a taxpayer receives a notice and is requested to respond or chooses to respond, the taxpayer must generally do so by mail. Through May 21, the IRS processed 5million taxpayer responses to proposed adjustments. It took an average of 251 days to do so – more than eight months. That is more than triple the processing time of 74 days in fiscal year 2019, the most recent pre-pandemic year. “When a math error or similar notice is generated in connection with a paper-filed tax return,” the report says, “the combination of the return processing delay and the correspondence processing delay may mean that the taxpayer must wait well over a year to get the issue resolved and receive the refund due.”

There are currently over 336,000 taxpayers who could not file their returns or receive their refunds because identity thieves had already filed a return using their identifying information. These taxpayers must submit affidavits and other documentation to substantiate their identities. They now generally must wait at least a year to receive their refunds. The IRS website states: “[D]ue to extenuating circumstances caused by the pandemic our identity theft inventories have increased and on average it is taking about 360 days to resolve identity theft cases.”

Telephone Challenges

During the 2022 filing season, the IRS received about 73 million telephone calls. Only one out of 10 calls reached an IRS employee. Compared with the 2021 filing season, IRS employees answered less than half as many calls, but the percentage of calls answered remained about the same because they also received less than half as many calls. The time the average taxpayer spent waiting on hold rose from 20 minutes to 29 minutes. A comparison of telephone service during the 2021 and 2022 filing seasons is shown in Figure 2.

Figure 2: IRS Enterprise Telephone Results Comparing Weeks Ending May 21, 2021, and April 23, 2022

“The combination of more than 21 million unprocessed paper tax returns, more than 14 million math error notices, eight-month backlogs in processing taxpayer correspondence, and extraordinary difficulty reaching the IRS by phone made this filing season particularly challenging,” Collins wrote.

TAS Objectives for FY 2023

As required by law, the Advocate’s report identifies TAS’s key objectives for the upcoming fiscal year. The report describes 14 systemic advocacy objectives, six case advocacy and other business objectives, and three research objectives. In light of the challenges taxpayers have been facing over the last two years, Collins wrote that TAS will be placing heavy emphasis on working with the IRS to improve the processing of tax returns and taxpayer service generally. Among the objectives the report identifies are the following:

- Automating the processing of paper tax returns. On March 29, as noted above, Collins issued a Taxpayer Advocate Directive (TAD) directing the IRS to implement scanning technology by the start of the 2023 filing season so that paper tax returns can be machine-read and employees will not have to keystroke each digit on the return into IRS systems. After obtaining an extension for responding, the IRS’s answer to the TAD is now due on Monday, June 27. IRS leaders have indicated they are not likely to implement 2-D barcoding, but Collins has strongly urged them to implement a plan to achieve automation of paper processing in time for the next filing season. “Doing so is critical,” Collins wrote. “It is unacceptable that the agency is still paying thousands of employees to keystroke the data from millions of tax returns, digit by digit, into IRS systems – creating the current processing backlog and producing an error rate in transcribing individual returns last year of 22 percent.”

- Reducing barriers to e-filing tax returns. Some taxpayers still prefer to file paper tax returns. However, many paper filers, perhaps the majority, would prefer to e-file their returns but are not able to do so. Among the barriers: some taxpayers must file IRS forms or schedules that the IRS does not accept through its e-file system; some taxpayers must include attachments (e.g., appraisals or disclosure statements) that cannot be filed by their tax software packages; some software packages block returns from e-file if the taxpayer overrides certain entries; IRS systems reject certain returns during the e-file process and require affected taxpayers to mail their returns instead; and some taxpayers live in areas of the country without broadband internet access or lack computer access and thus face greater difficulty in preparing and e-filing their returns. The report says the IRS must reduce e-filing barriers, so that more taxpayers can e-file and there will be fewer paper tax returns to transcribe or scan.

- Improving the IRS’s hiring and training processes. In FY 2022, Congress increased the IRS’s overall budget by almost 6% and the taxpayer services portion of the budget by nearly nine percent. Many of the IRS’s challenges stem from inadequate staffing, including limited staffing in Submission Processing and telephone call centers. The report says that hiring and adequately training new employees will enhance the taxpayer experience.

- Improving telephone service. Some taxpayer issues may be resolved through technology channels, and enhancing those channels must be a priority. But some issues are best resolved through a conversation, and some taxpayers are not comfortable with technology. The report says it is critical that taxpayers be able to reach the IRS by phone. As discussed above, IRS employees were only able to answer 10% of taxpayer telephone calls this filing season. “If a private company failed to answer nine out of 10 customer calls, customers would go elsewhere,” Collins wrote. “That, of course, is not an option for U.S. taxpayers, so it is critical that the IRS increase staffing in its telephone call centers to handle the volume of calls it receives.”

IRS Responses to National Taxpayer Advocate Administrative Recommendations

The National Taxpayer Advocate is required by statute to submit a year-end report to Congress that, among other things, makes administrative recommendations to resolve taxpayer problems. Section 7803(c)(3) of the Internal Revenue Code authorizes the National Taxpayer Advocate to submit administrative recommendations to the Commissioner and requires the IRS to respond within three months. Under this authority, the National Taxpayer Advocate annually transmits to the Commissioner all administrative recommendations proposed in her year-end report for response.

The National Taxpayer Advocate made 88 administrative recommendations in her 2021 year-end report and then submitted them to the Commissioner for response. The IRS has agreed to implement 61 (or 69%) of the recommendations in full or in part.

The IRS’s responses are published on the TAS website at https://www.taxpayeradvocate.irs.gov/arc-recommendations-tracker.

* * * * * * *

The National Taxpayer Advocate is required by statute to submit two annual reports to the House Committee on Ways and Means and the Senate Committee on Finance. The statute requires these reports to be submitted directly to the Committees without any prior review or comment from the Commissioner of Internal Revenue, the Secretary of the Treasury, the IRS Oversight Board, any other officer or employee of the Department of the Treasury, or the Office of Management and Budget. The first report must identify the objectives of the Office of the Taxpayer Advocate for the fiscal year beginning in that calendar year. The second report must include a discussion of the ten most serious problems encountered by taxpayers, identify the ten tax issues most frequently litigated in the courts, and make administrative and legislative recommendations to resolve taxpayer problems.

The National Taxpayer Advocate blogs about key issues in tax administration. Click here to subscribe. Past blogs from the National Taxpayer Advocate can be found here. For media inquiries, please contact TAS Media Relations at TAS.media@irs.gov or call the media line at (202) 317-6802.

About the Taxpayer Advocate Service

The Taxpayer Advocate Service (TAS) is an independent organization within the IRS that helps taxpayers and protects taxpayer rights. The local taxpayer advocate’s number is in local directories and at www.taxpayeradvocate.irs.gov/contact-us. Taxpayers can also call TAS toll-free at 877-777-4778. TAS can help those who need assistance in resolving an IRS problem, if the problem is causing financial difficulty, or those who believe an IRS system or procedure isn’t working as it should. This service is free. For more information about TAS and taxpayer rights under the Taxpayer Bill of Rights, go to www.taxpayeradvocate.irs.gov. Get updates on tax topics at facebook.com/YourVoiceAtIRS, Twitter.com/YourVoiceatIRS, and YouTube.com/TASNTA.